Taxpayers Deserve Answers – We’re Going to Get Them

Tuesday, County Judge Neal Franklin, retiring Commissioner John Moore, Commissioner Scott Herod, and Commissioner Ralph Caraway refused to support a $135K forensic and compliance audit on 2017 and 2021 Road Bond Projects. Since the County is sitting on tens of millions in unencumbered cash (over taxation), there was plenty of money to find answers.

It is clear they don’t want answers!

Only Commissioner Christina Drewry fought to get answers for you so that the County can fix this mess!

We spent hundreds of hours over the last 13 months inspecting County documents to get answers. What we found was horrifying—a case study in mismanagement! No oversight! Not even an update on the projects until we brought it up in Feb. 2025!

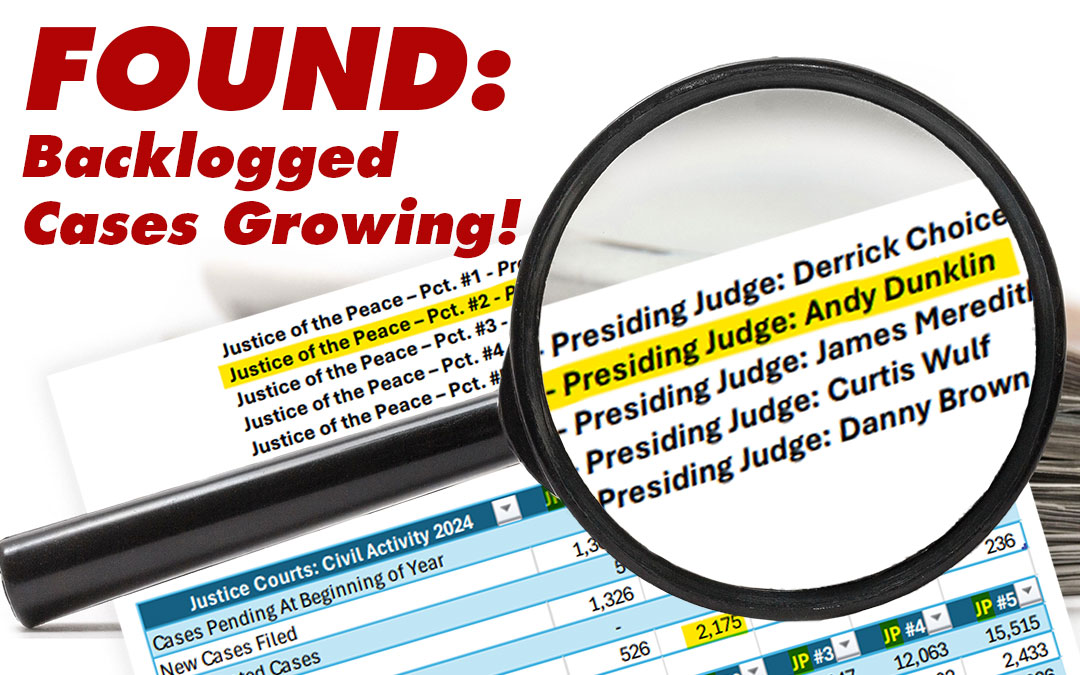

Smith County’s own records reveal:

🚨 Core Problems

- Massive Cost Overrun — A program sold as $84.5M is now projected at ~$185M. What caused overruns far beyond inflation?

- 5‑Year Plan Now in Year 12 — No timeline. No public discussion. Refuse to hold evening town halls. No plan to finish your roads.

- Regular Budgets Still Flowing — Road & Bridge received ~$120M in operating funds. Where are the improved pavement ratings?

- Untracked Supplements — $14.5M in extra appropriations show no audit trail.

⚠️ Quality & Documentation Failures

- Missing Engineering Records — No pre‑engineering, in‑project, post‑project, or warranty testing for 73% of the bond project files! The county engineer admitted he had no inspection documentation signing off on completed work!

- No Verification of Work — Claims that “only a few hundred dollars are unaccounted for” are false, but also ignore the real issue: There’s no documentation to prove many roads were repaired or met standards.

🚧 Questionable Use of Bond Funds

- Bond Money Diverted — $3.2M in bond funds went to a new road (Centennial Blvd.), not existing roads as promised.

- Unauthorized Projects — 25 projectscharged to Phase 1 weren’t on any Commissioners Court approved priority list.

- Policy Violated — These projects were sold to the voters as reconstruction projects with external contractors for arterial/collector roads with the Road & Bridge Department refocusing on maintaining and repairing roads. The County broke this promise.

- “In‑House” Work Billed to Bond — County crews rebuilt roads internally while charging only materials to the bond (not labor & equipment) — hiding the true cost to taxpayers…but worse…

- Missing Purchase Orders — $8.2M in purchase orders for “in‑house” work had no discoverable audit trail!

📉 Misreported Deliverables

- Reconstruction Miles Overstated — Smith County claimed 99.7 miles of reconstruction. Atkins Engineering records show only 55 miles were true reconstruction — the rest were overlays.

Bottom line:

This isn’t transparency.

This isn’t accountability.

And it certainly isn’t over!

Grassroots America will not “move on” until the Commissioners Court explains how they plan to fix this!

Taxpayers deserve better.

Dumping any more tax dollars into Road & Bridge without reforming the entire thing from top to bottom is like flushing your tax dollars down a sewer! Stay tuned! We aren’t done with this!